How AI is Disrupting Your Business Model

Not affiliated with Board of Innovation · Built from the public webinar

Most companies are treating AI as a productivity tool. That's not wrong, it's just incomplete. This guide breaks down Laura Stevens' webinar into the frameworks, examples, and questions worth sitting with.

Laura Stevens | Managing Director, Board of Innovation

Executive Summary

AI is not disrupting industries the way most executive teams think it is.

The comfortable story: deploy some co-pilots, run some pilots, create a use-case task force. That's not wrong. It's just not enough.

Laura Stevens, Managing Director at Board of Innovation, argues that AI belongs in the same category as electricity and the internet: a general purpose technology that doesn't just improve existing processes but reshapes entire industries. Every general purpose technology in history has done three things: enabled new business models, restructured cost bases, and redefined what competitive advantage means.

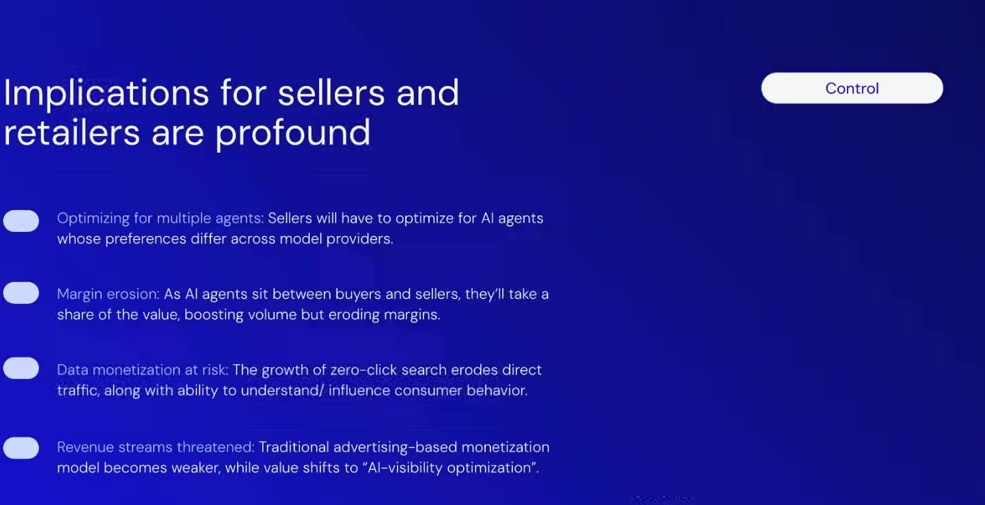

In the webinar, Stevens maps three structural disruptions already underway. First, control is shifting from human buyers to algorithmic intermediaries. If you don't feature in the algorithm, you don't exist in the market. Second, barriers to entry are collapsing. AI-native companies are being built by teams of eight that would previously have required hundreds. Third, customers are changing what they'll pay for. When AI can produce a market analysis in minutes, the era of billing for effort is over.

The response is not more use cases. It's rethinking where value sits, how it's monetised, and what makes your business hard to replace.

Use this guide as a briefing document, a starting point for a board conversation, or a lens for your AI strategy review.

Quick Take TL;DR

The full webinar distilled into six themes. Each card shows one key point; click to reveal the rest.

The Big Picture

- Most enterprise AI strategies are a list of use cases. That's operational thinking applied to a structural problem.

- AI is a general purpose technology, comparable to electricity or the internet, not a software upgrade.

- General purpose technologies always do three things: create new business models, change cost structures, shift the basis of competitive advantage.

- Treating AI as a toolbox upgrade means optimising a model that may no longer hold.

Control Shifts

- Three structural disruptions are already underway: control shifts, competition increases, value moves.

- Control is shifting from human buyers to the algorithms that mediate decisions.

- Customers increasingly start their buying journeys in ChatGPT or Perplexity, not brand websites.

- If your brand isn't surfaced by the algorithm, you may not be considered at all.

- The next phase: AI doesn't just shape decisions, it executes them. Agentic commerce is already live.

- Agent-to-agent commerce is coming. Your AI will negotiate with brand AIs, with no human in the loop.

Competition Collapse

- Suppliers are becoming interchangeable faster. Switching costs drop. Brand loyalty weakens. Performance metrics dominate.

- AI is also removing entire market layers, specifically those that only add coordination or production without owning defensible assets.

- Not all intermediaries are threatened equally. Booking.com, for example, owns data, APIs, payments and distribution: a defensible position.

- AI dramatically lowers barriers to entry. New competitors are being built AI-native, leaner, and at a structurally lower cost base.

- A developer built a company of 8 people, reached 250K users, hit $3.5M ARR, and sold for $80M. In six months, with no outside capital.

- Basis AI reached a $1B valuation with a fraction of the headcount traditional service firms require.

Value Migration

- The third disruption: customers are shifting from paying for effort to paying for outcomes.

- When AI can generate a market analysis in minutes, the premium on human-delivered reports collapses.

- Billing by the hour is becoming structurally indefensible. Junior leverage models in consulting are under pressure.

- Asset-based businesses are shifting from selling products to selling outcomes: uptime guarantees, performance contracts, power-by-the-hour.

- SaaS is under pressure from both sides: supply (easier to build alternatives) and demand (fewer seats needed when AI amplifies small teams).

Exposure & Defense

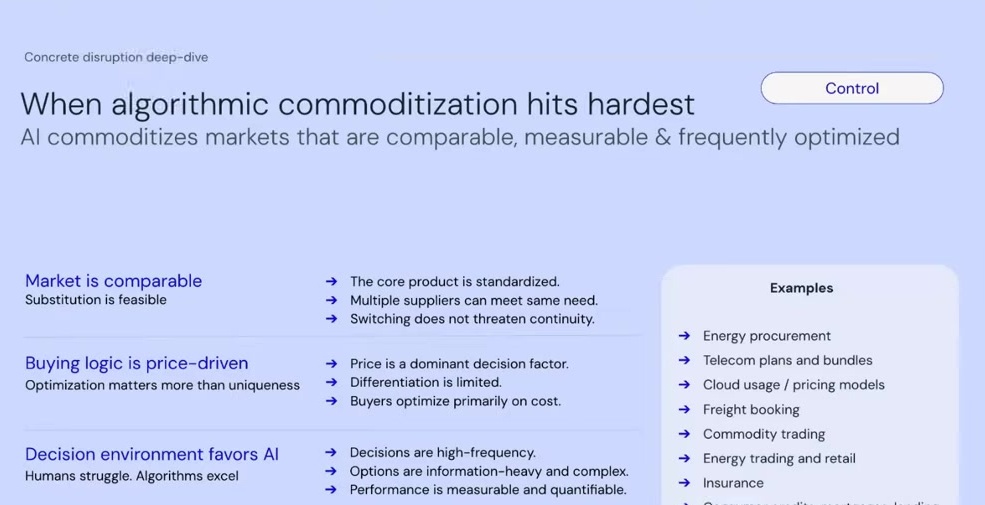

- Industries most vulnerable: those where products are comparable, price-dominant, and decisions are high-frequency.

- Telecom bundles, energy procurement, cloud usage, insurance: prime candidates for AI-driven commoditisation.

- Regulation delays disruption. It doesn't prevent it.

- Defensible positions in an AI world: proprietary data, deep workflow integration, differentiated personalised experience.

- A Dutch entrepreneur turned down a ~$500M acquisition from OpenAI for his gaming behavior dataset. Proprietary data is a moat.

The Response

- An AI strategy is not a use-case list. It must address business model reinvention, workflow redesign, and operating model transformation.

- Three transformation tracks: Strategic Reinvention, Workflow Redesign, Operating Model Redesign.

- The mindset that makes the difference: willingness to step outside incremental optimisation and question whether the model itself still holds.

The Argument in Three Acts

The Problem

Most companies treat AI as a productivity tool. That's a category error. AI is a general purpose technology, like electricity or the internet, that rewrites business models, cost structures, and competitive advantage. Optimising your existing model is not a strategy.

The Disruption

Three forces are already reshaping markets. Algorithms now control the customer journey, not brands. AI-native startups with 8 people outcompete teams of 200. And customers are shifting from paying for effort to paying for outcomes. Billing for hours is ending.

The Response

Score your vulnerability across 8 dimensions with the AI Disruption Index. Then act on three tracks: reinvent your business model, redesign workflows around AI capabilities, and transform your operating model from pyramid to AI-augmented structure.

Most companies are solving the wrong problem.

Walk into any large enterprise today and ask about their AI strategy. You'll hear about co-pilot rollouts, productivity pilots, use-case registries, and training programmes. These things are real. They produce real results. And they're not sufficient.

Laura Stevens calls this the "comfortable illusion": the idea that AI is primarily a tool for making your existing operating model more efficient. The problem isn't that this is wrong. The problem is that it's a category error. Optimisation is an operational question. AI is a structural one. Applying operational logic to a structural shift means you're refining a model that may soon stop making sense entirely.

The deeper issue: a structural shift cannot be addressed with incremental logic. If competitors are rethinking their business models from scratch, then being incrementally more efficient inside your current model is not a strategy. The gap between "we're running pilots" and "we're rebuilding how we compete" is not one you close with a task force.

"A structural shift can never be addressed with an incremental logic, which is unfortunately what we often see in companies. And so treating AI as a toolbox upgrade really misses that bigger redesign opportunity."

Laura Stevens, Managing Director, Board of InnovationAudit your current AI strategy. If it reads like a project list, it probably is one. The test: does your strategy address where you play, how you win, and what makes you defensible? Or does it address where you can shave cost and speed up processes? Both matter. Only one is strategic.

Think electricity, not software. The frame changes everything.

The category you put AI into determines the strategy you build. If it's a software category, you buy tools, run projects, and manage change. If it's a general purpose technology, the category that includes electricity and the internet, the response looks completely different.

General purpose technologies don't improve existing processes. They reshape industries. The internet didn't create faster mail. It created e-commerce, social media business models, and the destruction of entire sectors of the economy. Electricity didn't create better candles. It rewired how manufacturing worked, how cities were built, how labour was organised. Stevens' argument is that AI belongs in this category, and that history gives us a reliable map of what comes next.

That map has three consistent features. First, entirely new business models emerge: not better versions of what exists, but fundamentally different ways of creating and capturing value. Second, cost structures change: when tasks that required time and expertise can be automated and delivered at scale, they become dramatically cheaper to produce. Third, the basis of competitive advantage shifts. Capital, size, brand, and reach become less decisive. Proprietary data, process integration, and algorithmic ownership become more so.

New Business Models

Not better versions of what exists. Fundamentally different ways of creating and capturing value.

New Cost Structures

Tasks requiring time and expertise become dramatically cheaper to produce at scale.

New Competitive Advantage

Proprietary data, process integration, and algorithmic ownership replace capital and brand.

"AI is not just a tool but something that economists call a general purpose technology, which is much more similar to the internet or to electricity. And we know that these technologies did not just improve existing processes; they reshaped entire industries."

Laura Stevens, Managing Director, Board of InnovationRun a thought experiment with your executive team. If AI does to your industry what the internet did to retail, what survives? What disappears? What new model wins? This is not a futurism exercise. It's a stress test. The companies that ran it about digital fifteen years ago are now the incumbents. The ones that didn't are mostly gone.

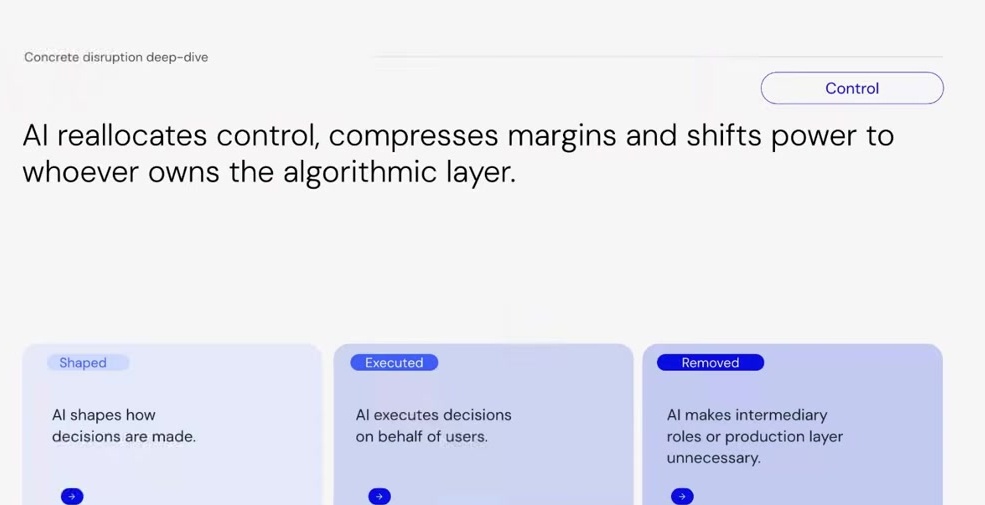

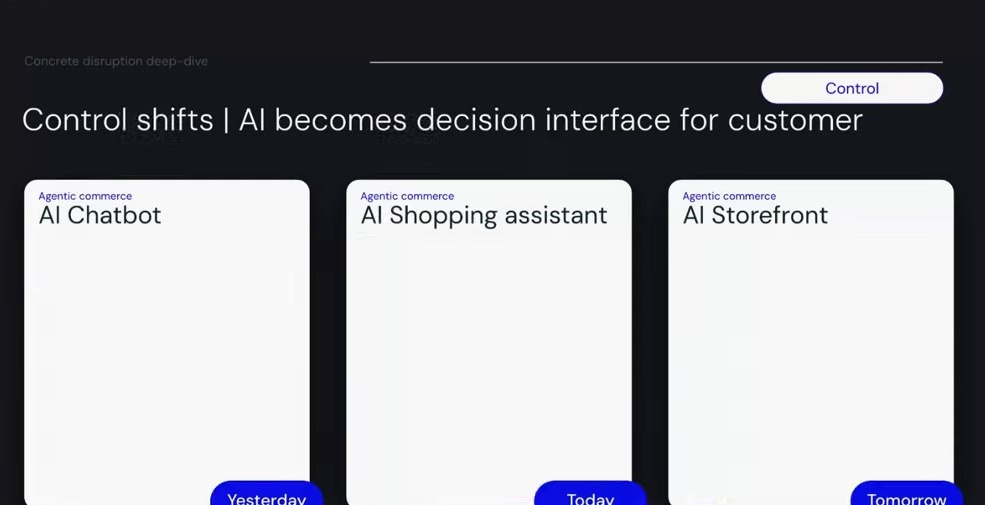

If you don't control the algorithm, you don't control the customer.

Markets have always been built around human buyers: impulsive, brand-influenced, limited in how much they can process. Every aspect of how businesses win customers rests on that assumption. AI is dismantling it.

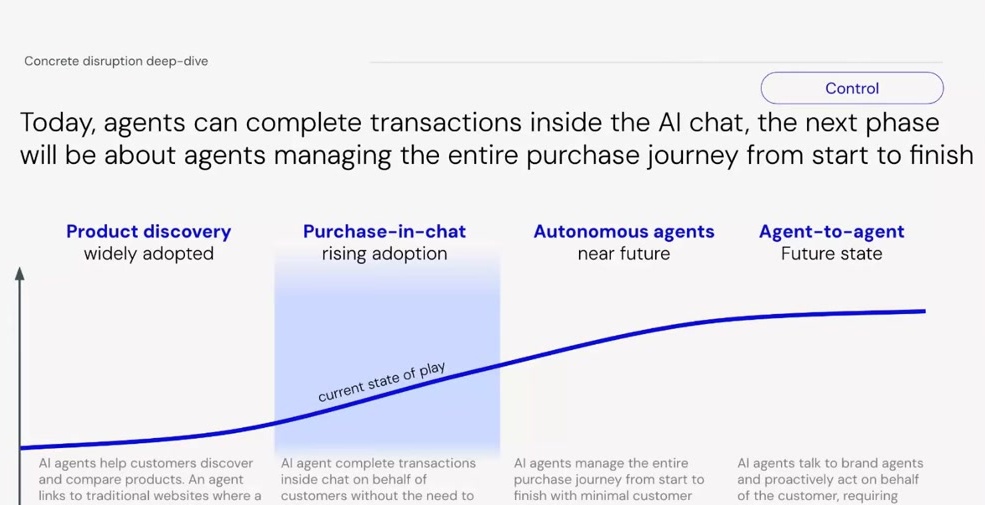

Customers increasingly begin their journeys not on brand websites but in ChatGPT, Perplexity, or AI-powered search. They ask "what's the best CRM for a mid-sized company?" or "which laptop is best under a thousand euros?" and the algorithm summarises, compares, filters, and recommends. Humans still make the final call, for now, but the consideration set and how options are framed is shaped entirely by a system that didn't exist five years ago. If you're not in that set, you're not in the race.

The disruption deepens as AI moves from shaping decisions to executing them. Agentic commerce is already live in the US, with AI assistants completing purchases inside chat interfaces. The trajectory: autonomous agents that manage the full journey from discovery to checkout, followed by agent-to-agent commerce where your AI negotiates with brand AIs, no human involved. At that point, the interface becomes the decision maker. Brands aren't competing for attention. They're competing to be selected by a system.

"Brands are no longer competing for shelf space; they are competing to be selected by the agent."

Laura Stevens, Managing Director, Board of InnovationWhere does your brand show up when an AI summarises your category? Test it. Open ChatGPT or Perplexity and ask what your target customer asks. If you're not appearing, or appearing unfavourably, that's a positioning problem with a structural cause. Longer term, your go-to-market needs a position on agentic commerce: how will you optimise for selection by AI agents, not just visibility to human eyes?

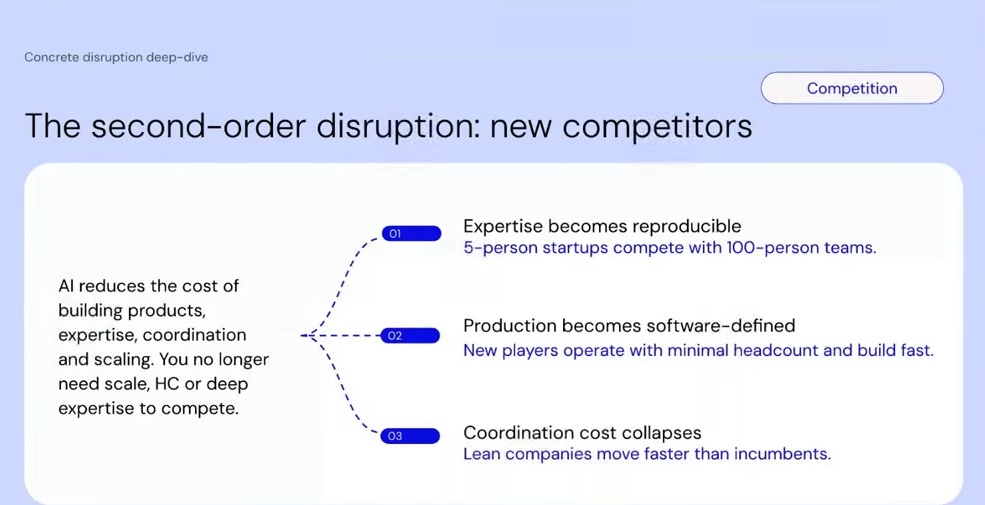

Your most dangerous competitor probably has a team of eight.

Competitive moats have traditionally relied on scale: large teams, capital, deep expertise, long development cycles. AI is compressing all of that. What once required 50 engineers and months of work can now be built by a small team in weeks.

This is already happening. Stevens points to B44: built by a developer as a side project using AI-assisted "vibe coding." In six months, with no outside funding, the company reached 250,000 users, hit $3.5 million in annual recurring revenue, and sold for $80 million. The team? Fewer than ten people. Basis AI tells a similar story: a $1 billion valuation with a fraction of the headcount a traditional services business would need, built on autonomous agents handling end-to-end accounting.

The implication isn't just that new entrants are more dangerous. It's that the cost of building alternatives to your product is falling continuously. More competitors enter, and customers become less willing to pay premiums when they know alternatives are cheap to build. The question is whether your strategy accounts for that.

Two companies that illustrate the new competitive reality. Both built by tiny teams, both powered by AI.

B44

A side project built with AI-assisted "vibe coding." No VC, no large team. Reached 250,000 users in six months and sold for $80M.

Basis AI

An AI-first accounting firm using autonomous agents for end-to-end tasks. Reached $1B valuation with a fraction of traditional headcount.

"When the cost of building drops, barriers to entry fall and competition increases."

Laura Stevens, Managing Director, Board of InnovationMap your barriers to entry honestly. Which moats depend on capital, headcount, or expertise that AI is commoditising? Which depend on proprietary data, workflow integration, or accumulated customer relationships? The first category is shrinking. The second is where defensibility lives.

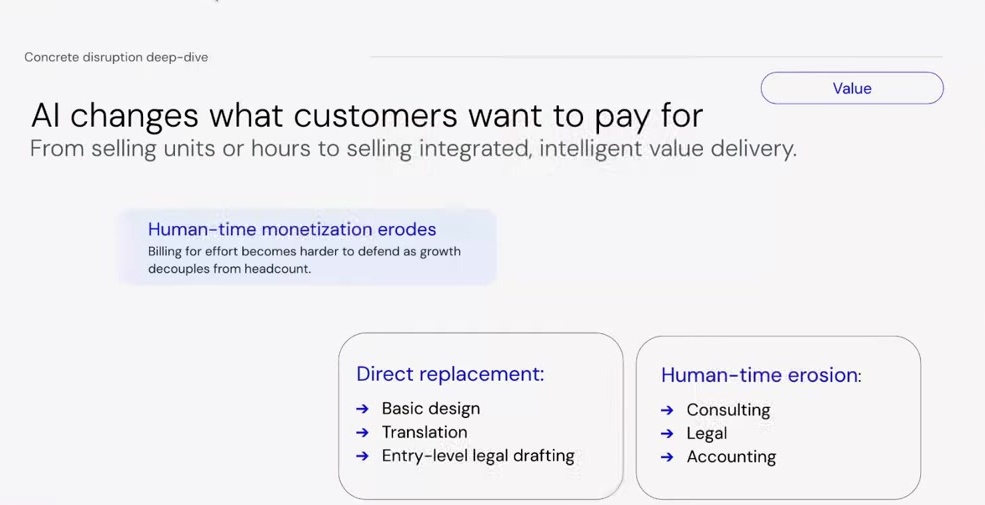

When AI can write the report in minutes, no one is paying five thousand euros for it.

Most business models rest on a simple premise: revenue scales with effort. You charge by the hour, by the seat, by the deliverable. AI doesn't just make that effort cheaper to produce. It breaks the logic that made effort valuable in the first place.

Stevens puts it simply: if AI can generate a market analysis in minutes, why would a client pay five thousand euros for one? The pressure shows up everywhere. In professional services, it hits the junior leverage model hardest: AI automates exactly the repetitive cognitive tasks that junior analysts were hired to do, compressing billable hours and shrinking the traditional pyramid. In SaaS, it hits seat-based pricing: if AI lets three people do the work of twenty, you're selling eighteen fewer seats.

The response is not to defend the old model. It's to understand what customers will actually pay for when effort becomes cheap. The answer, consistently, is outcomes. Rolls-Royce doesn't sell jet engines. It sells hours of thrust. That logic is spreading across services, manufacturing, and beyond.

"When the cost of producing knowledge drops, the willingness to pay for that production drops as well. Customers shift from paying for effort to wanting to pay for outcomes or real impact."

Laura Stevens, Managing Director, Board of InnovationWhat are you actually charging for: effort or outcomes? If effort, which parts can AI replicate at near-zero marginal cost? That's where your pricing model is exposed. The harder question: what does your customer actually value, separate from the labour required to produce it? That answer shapes the redesign.

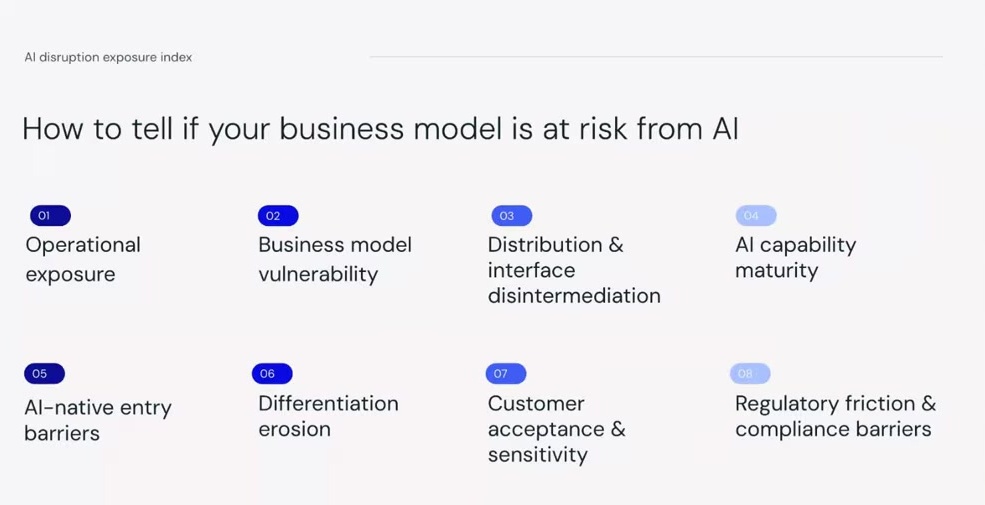

Is your business model at risk?

BOI's AI Disruption Exposure Index scores vulnerability across eight dimensions. Each represents a surface where AI-driven disruption can hit your business.

Operational Exposure

How template-driven, repetitive, and information-handling-heavy is the work?

Business Model Vulnerability

How tied is revenue to human time and scarce expertise?

Distribution Disintermediation

Is your offering comparable, price-driven, and low-risk for AI-mediated switching?

AI Capability Maturity

How well can current AI perform core industry tasks right now?

AI-Native Entry Barriers

How easy is it for a lean AI-native competitor to enter your market?

Differentiation Erosion

Can your differentiation survive AI replication?

Customer Acceptance

How comfortable are customers with AI replacing humans in your domain?

Regulatory Friction

Does regulation slow disruption? Note: this is a delay mechanism, never a permanent shield.

This is not a use-case problem.

The failure mode Stevens sees most often: companies respond to structural disruption with operational tools. They build use-case lists. They deploy co-pilots. They run pilots. None of this is wrong, but it's insufficient when the disruption is structural. The question is not which processes to automate. It's whether the model those processes serve still holds.

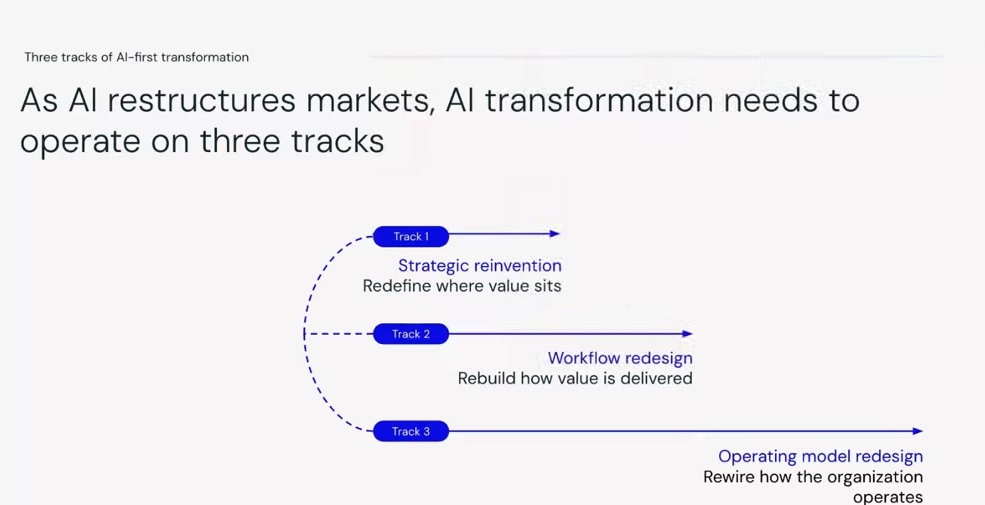

BOI's framework organises the response into three tracks. Strategic reinvention: where do you play, how do you win, what makes you hard to replace? Workflow redesign: which workflows are high-volume, labour-intensive, and repeatable enough that an AI-first redesign changes your cost base structurally? Operating model redesign: as delivery changes, so must structure, governance, roles, and culture.

Defensible positions, Stevens argues, cluster around three things: proprietary data that others cannot replicate, deep integration into customer workflows that raises switching costs, and differentiated experiences that make comparability harder. A Dutch entrepreneur turned down a ~$500 million offer from OpenAI for his gaming behaviour dataset. Data is a moat. Integration is a moat. Generic output is not.

Strategic Reinvention

Redefine where value sits. Where is your model vulnerable? What makes you hard to replace? How do you monetise in an outcomes-driven world?

Workflow Redesign

Rebuild how value is delivered. Which workflows are repeatable, high-volume, labour-intensive? What can be structurally redesigned?

Operating Model Redesign

Rewire how the organisation operates. Governance, roles, culture, skills, capabilities: all must evolve.

"If your AI strategy today is a list of use cases, if it's only about co-pilots or shallow tools or use case implementation, then you're most likely trying to optimize a business and an operating model that will no longer hold in the future."

Laura Stevens, Managing Director, Board of Innovation"AI is not a technology shift. It is a market shift. And market shifts don't reward optimization; they reward reinvention."

Laura Stevens, Managing Director, Board of InnovationQ&A Highlights

The window is open.

The companies winning in AI-disrupted markets right now aren't necessarily the biggest or best-resourced. They're the ones that got honest about their exposure early and started redesigning before disruption forced their hand.

Laura Stevens and the Board of Innovation team work with organisations ready to have that conversation at a structural level.